Payroll reports

Make smarter business decisions with advanced payroll reporting. It shows where money’s spent, highlights trends and supports better budgeting. With the right payroll reports, employers can plan ahead, manage costs and stay in control of their workforce.

Real-time payroll reporting gives access to monthly, annual and employee payroll reports when they’re needed most. Custom payroll reports support financial forecasting, HR planning and HMRC annual payroll reporting. Online access makes it easy to stay compliant and avoid mistakes or penalties.

What is payroll reporting and why does it matter?

Good payroll reporting helps your business stay in control of one of your biggest costs - labour. It supports fair pay, accurate budgeting and better workforce planning. With clear payroll activity reports, employers can track overtime, spot patterns and see exactly where money is going. Decisions will be improved across HR, finance and leadership teams with better payroll data.

PayCaptain’s payroll reporting software makes this easier by automating reports and showing real-time data. It speeds up payroll approvals and ensures compliance with HMRC. Regular payroll data analysis highlights trends and issues early, helping businesses plan ahead with confidence.

Types of payroll reports for every business need

Payroll reports help employers understand costs, track changes and stay compliant. PayCaptain’s payroll reporting software has a wide range of standard payroll reports to suit the needs of HR, finance and leadership teams. Custom reports can be built quickly and easily for deeper analysis.

Payroll management reports

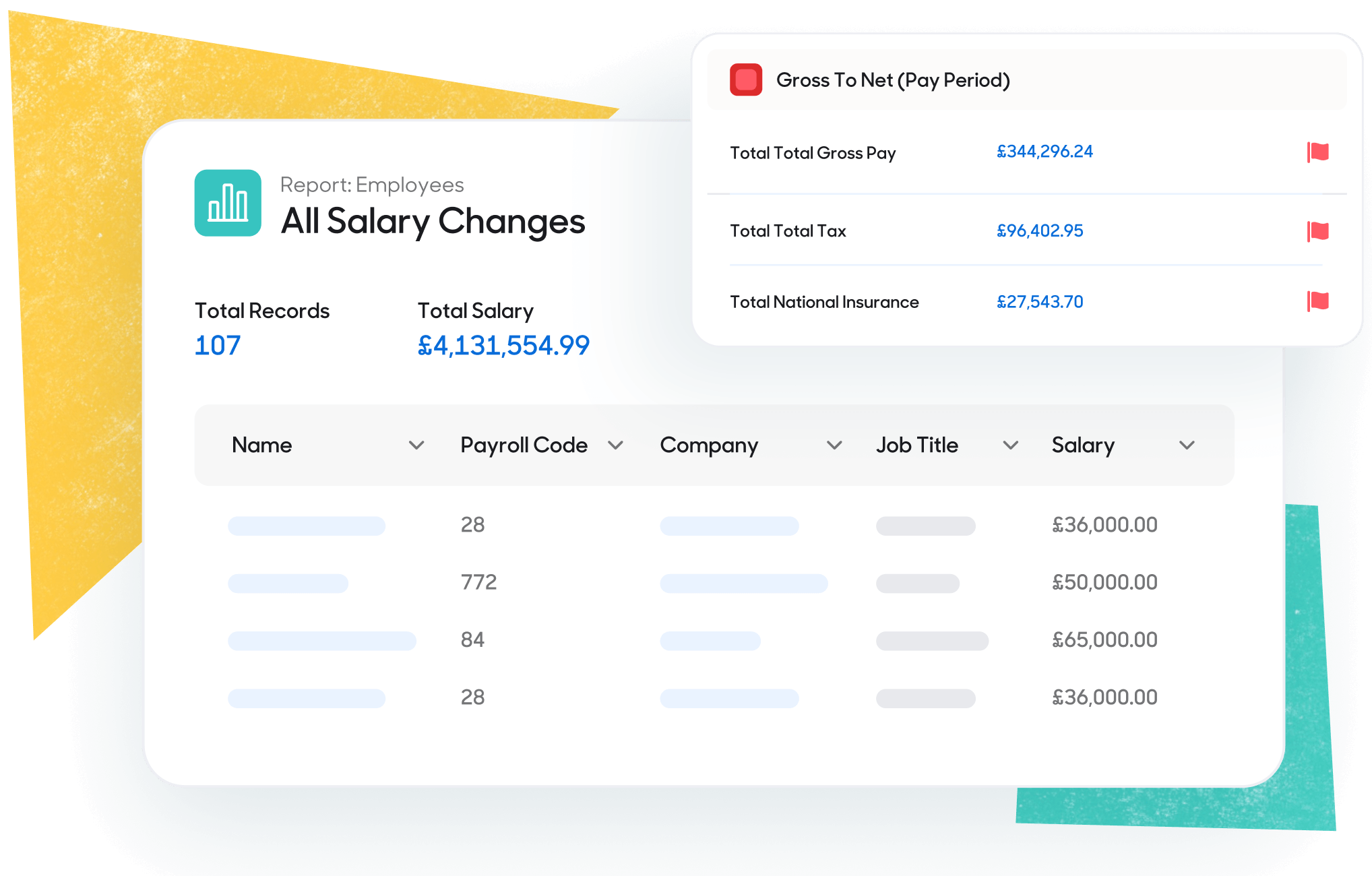

Supporting payroll approvals and tracking overall payroll costs, these reports include journals and detailed audit trail reports. Payroll activity - both before and after payroll is processed - can be monitored. These reports help teams check accuracy, explain payments and stay in control of spending.

Monthly payroll reports

Monthly reports include FPS and EPS submissions required by HMRC under Real Time Information rules. They also show gross to net figures, pension contributions, employee payments and any exceptions that need attention.

Annual payroll reports

End-of-year reports include the final FPS, employment summaries and certified submissions to HMRC. P60s and P11Ds are generated for employees, and gender pay gap reporting is included where required.

Overtime and absence reports

Providing a clear breakdown of how much overtime is being worked and when employees are off, tracking this data helps employers manage workloads and identify trends that may need action.

Headcount and departmental cost reports

Supporting better resource planning and cost control, these reports show how many people are working in each area of the business and how much each department costs.

Cost of employment reports

Improving budgeting and financial planning by getting a full picture of what it costs to employ staff, including wages, pensions and benefits.

Pension and PAYE/NIC reconciliation reports

Avoid compliance issues and errors by ensuring all contributions and deductions match what’s been reported and paid.

New starter and leaver reports

Improve onboarding, offboarding and keeping employee records up to date with payroll reports that track people joining or leaving the business.

Holiday accrual reports

Plan cover and manage leave balances more accurately with detailed reports that show how much holiday has been earned but not yet taken.

Workforce analytics reports

Support strategic planning and help improve employees’ experiences with custom payroll reports that give insight into workforce trends. Employee turnover, pay levels and financial wellbeing tool usage can all be analysed.

Benefits of payroll reports

Keeps your business compliant

Payroll reports help employers meet all HMRC requirements, including real-time information submissions and annual reporting. With PayCaptain’s payroll insights software, key reports like FPS, EPS, P60s and P11Ds are generated automatically and submitted on time. This reduces the risk of mistakes, missed deadlines and costly penalties. Keeping accurate payroll management reports also supports audit readiness and compliance with payroll tax reporting rules.

Saves time

Automated payroll reporting removes the need for manual checks and spreadsheets. PayCaptain’s payroll reporting software delivers monthly and annual reports instantly, with data pulled directly from payroll activity. This speeds up the approval process and supports real-time payroll reporting. It ensures accurate submissions to HMRC with minimal admin.

Builds trust

When payroll is accurate, timely and transparent, employees feel more confident in how they’re paid. Clear employee payroll reports show pay, tax, deductions and benefits in one place. With online payroll reports and easy access to past records, questions can be answered quickly and easily. PayCaptain’s reporting helps build open communication around pay, improving trust across the workforce.

Saves money

One of the key benefits of payroll reporting is cost control. With access to payroll analysis reports, employers can track overtime, monitor staffing costs and identify overspending. Custom payroll reports highlight where resources are stretched or underused. PayCaptain’s payroll insights software supports smarter budgeting and helps reduce waste by improving how people are managed and paid.

Improves decision-making

Good data leads to better decisions. Payroll reporting shows real trends in headcount, turnover, absence and department costs. Reports can be filtered and customised to support HR planning, finance reporting or leadership decisions. From holiday accrual to departmental spend, PayCaptain’s payroll reports help employers act on what the numbers are really saying.

How to create payroll reports

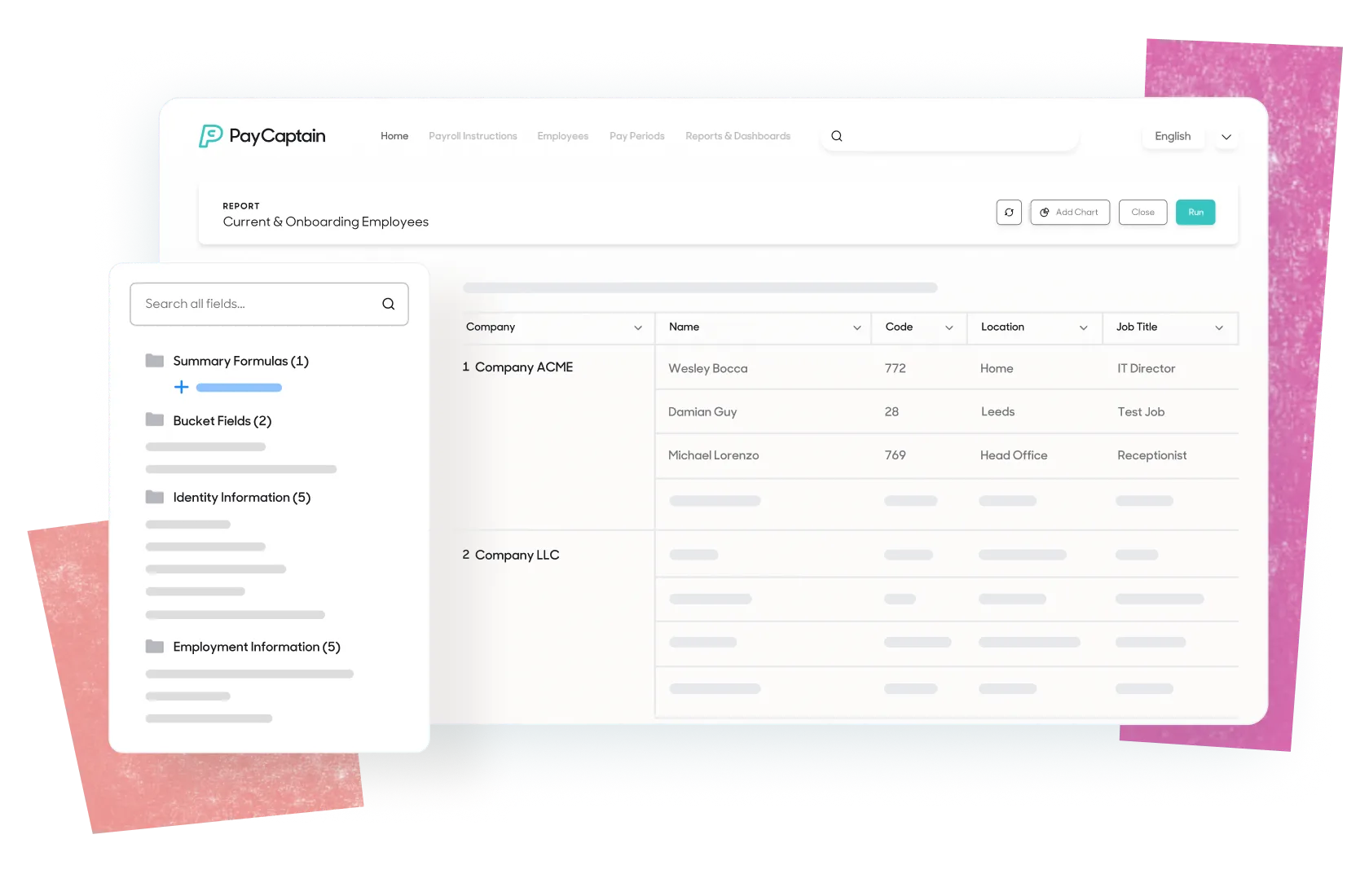

Creating payroll reports with PayCaptain is quick, simple and doesn’t require specialist support. The built-in report-builder groups and summarises payroll data into clear, standard reports. And it’s all available at the touch of a button. Employers can instantly see key payroll information like employee payments, pension contributions, departmental costs and payroll exceptions.

Data is easy to read with built-in graphs and visual tools. These can be added to any report to help show trends, patterns and changes over time. Whether it’s tracking overtime, viewing absence trends or monitoring costs, visual reports make it easier to understand the numbers and take action.

New custom reports and payroll dashboards can be created in-house. No technical skills are needed and users have full control. Report templates can be adjusted, filters added and layouts changed to meet your business needs. PayCaptain’s payroll reporting software puts powerful payroll data into the hands of those who need it, when they need it.

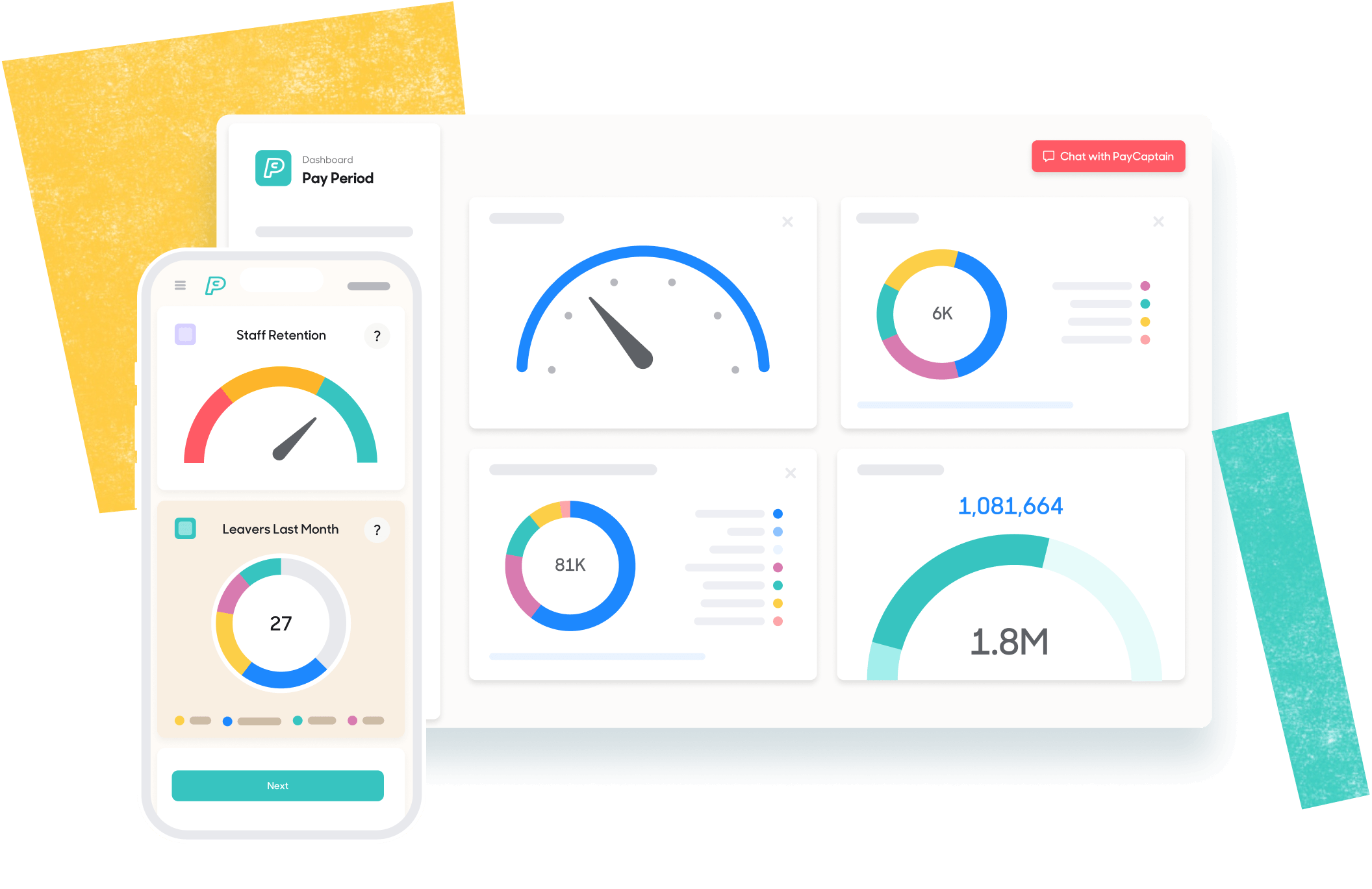

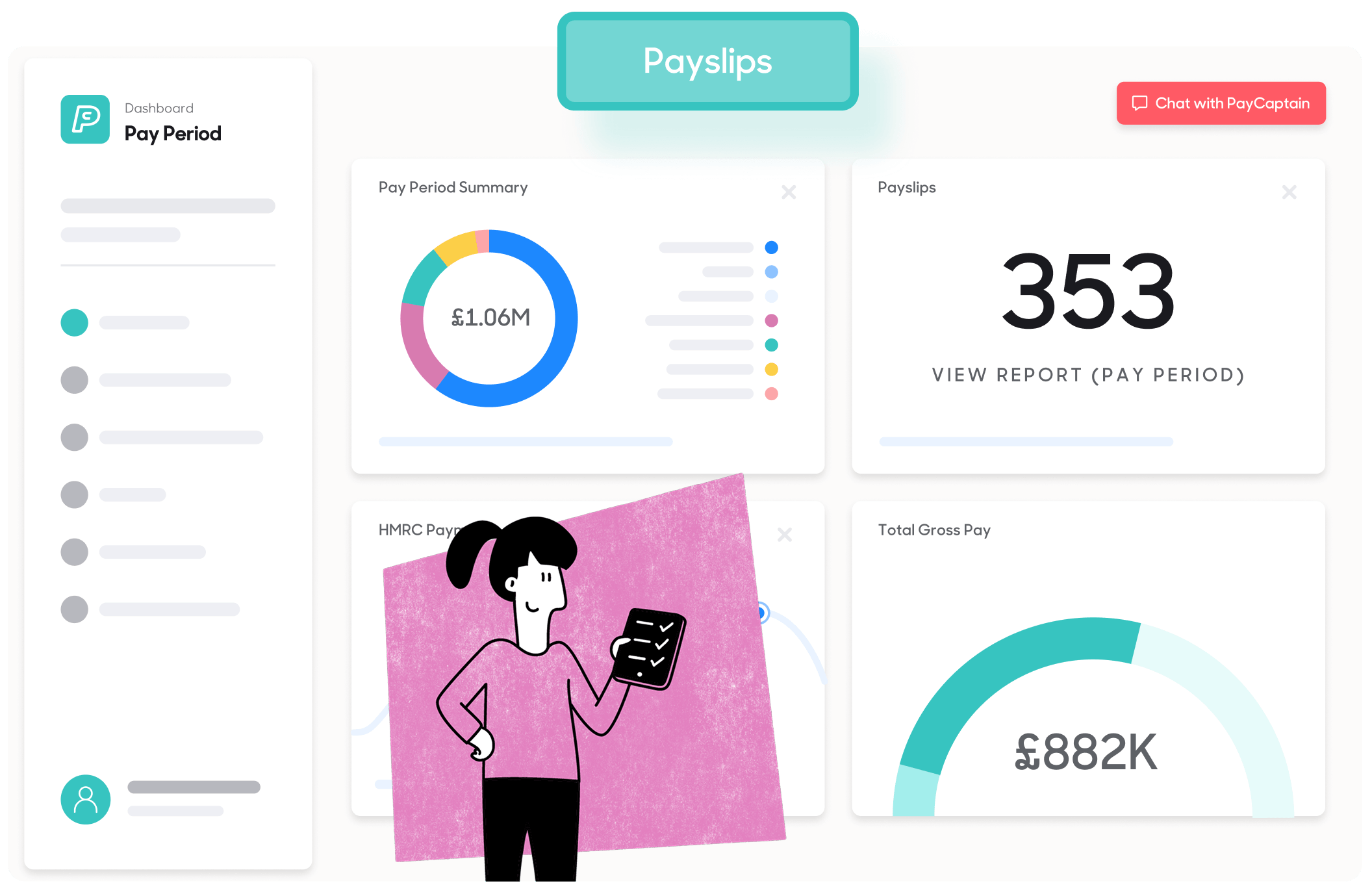

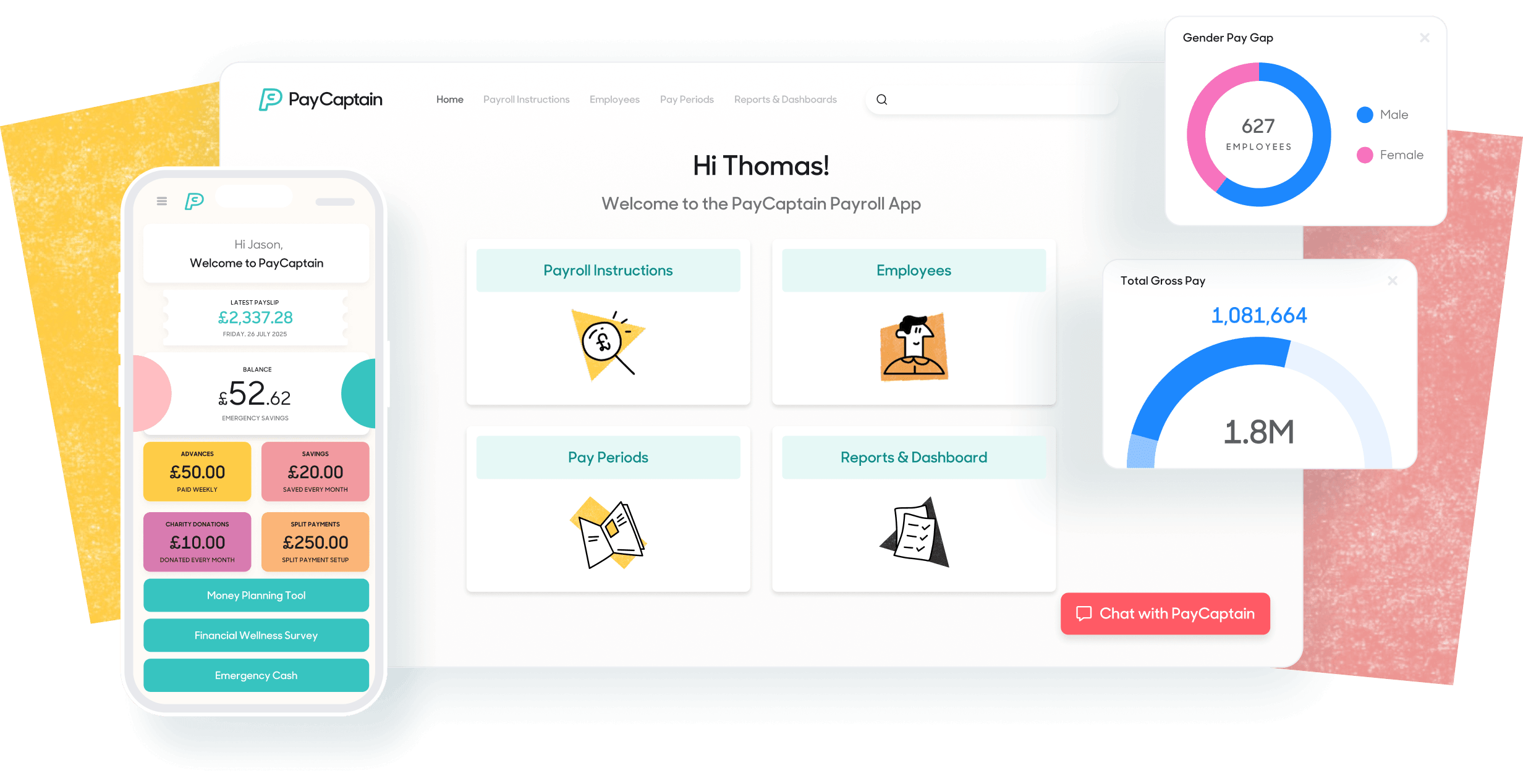

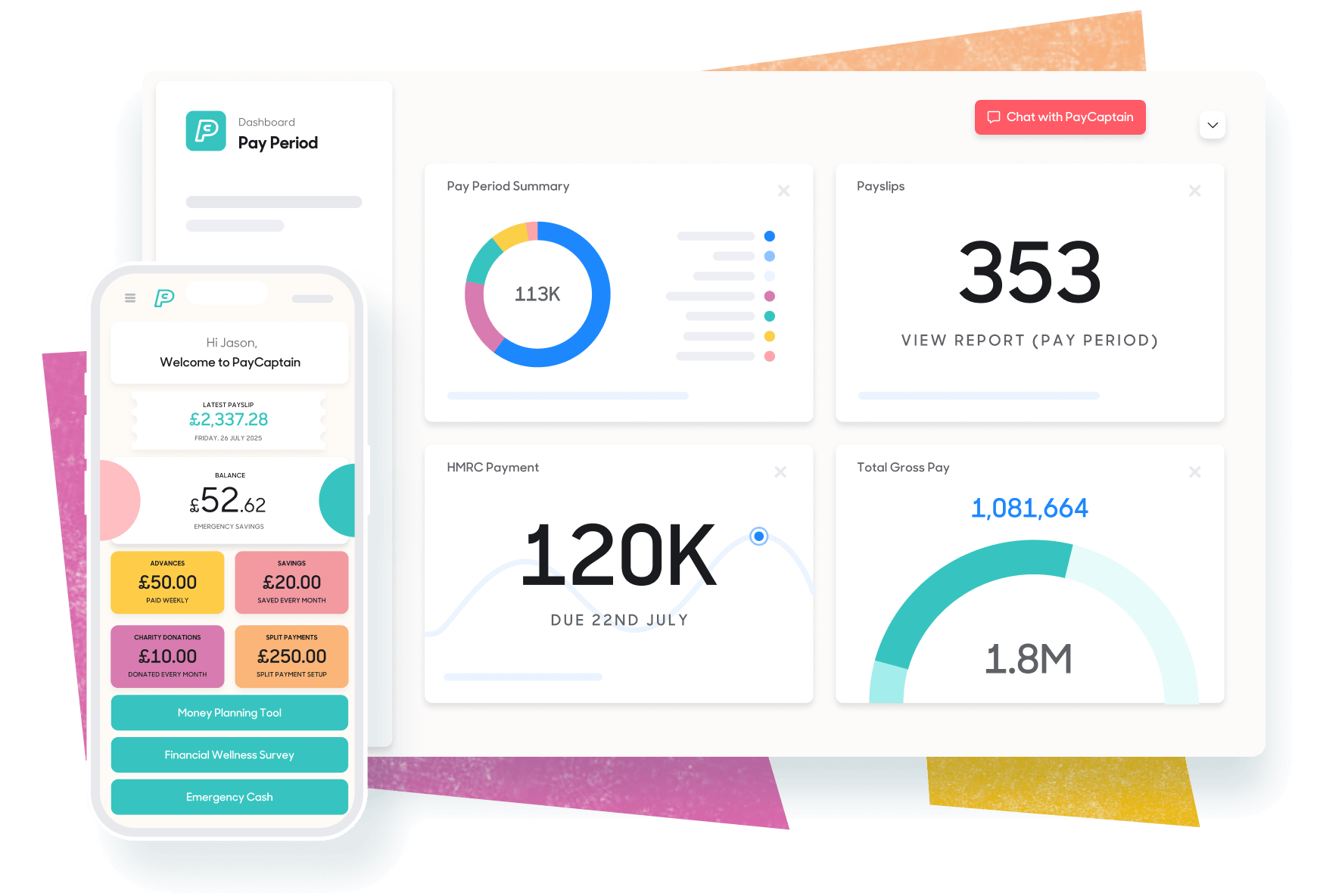

Payroll reports dashboard

See the full picture of your workforce and payroll at a glance. Make faster decisions, respond to issues early and manage people more effectively. PayCaptain’s payroll dashboard software gives HR, finance and leadership teams instant access to real-time payroll reporting and key HR statistics.

Interactive dashboards display live data on staff turnover, retention, length of service, reasons for leaving and workforce demographics. They also show payroll costs, gross to net pay, departmental spend and other key metrics. With visual graphs and filters, large datasets become easy to understand and act on.

Dashboards help maintain clean, accurate data by flagging missing or unusual entries. Built-in data integrity tools and exception reports support compliance and reduce the risk of errors. With everything in one place, PayCaptain’s payroll reporting software makes it easier to track trends, plan ahead and stay in control.

Secure and compliant payroll reporting

Stay compliant and protect sensitive data with confidence. PayCaptain’s payroll reporting software helps employers meet UK payroll regulations and keep employee information secure – without any extra work.

By automating key payroll reports and applying strong security measures, businesses can reduce risk and avoid penalties. It’s a straightforward way to stay in control of payroll reporting while meeting legal and data protection standards.

How to meet UK payroll reporting rules with confidence

Accurate, automatic and on time, PayCaptain takes the pressure off payroll compliance.

Employers never miss a submission or deadline as RTI reporting is handled automatically. Built-in checks in the AI-powered payroll reduce the risk of errors before reports go to HMRC. Pension auto-enrolment is fully managed, helping ensure all eligible employees are enrolled correctly and contributions are reported without delay.

Sensitive data is protected at every step, supporting full GDPR compliance and reducing the risk of data breaches. There’s no need to manually track changes to tax rules - PayCaptain’s HMRC-recognised payroll software automatically stays up to date, so payroll reporting always meets current legal requirements.

By building compliance into every step, PayCaptain helps employers avoid penalties, reduce admin and stay confident they’re meeting all legal obligations.

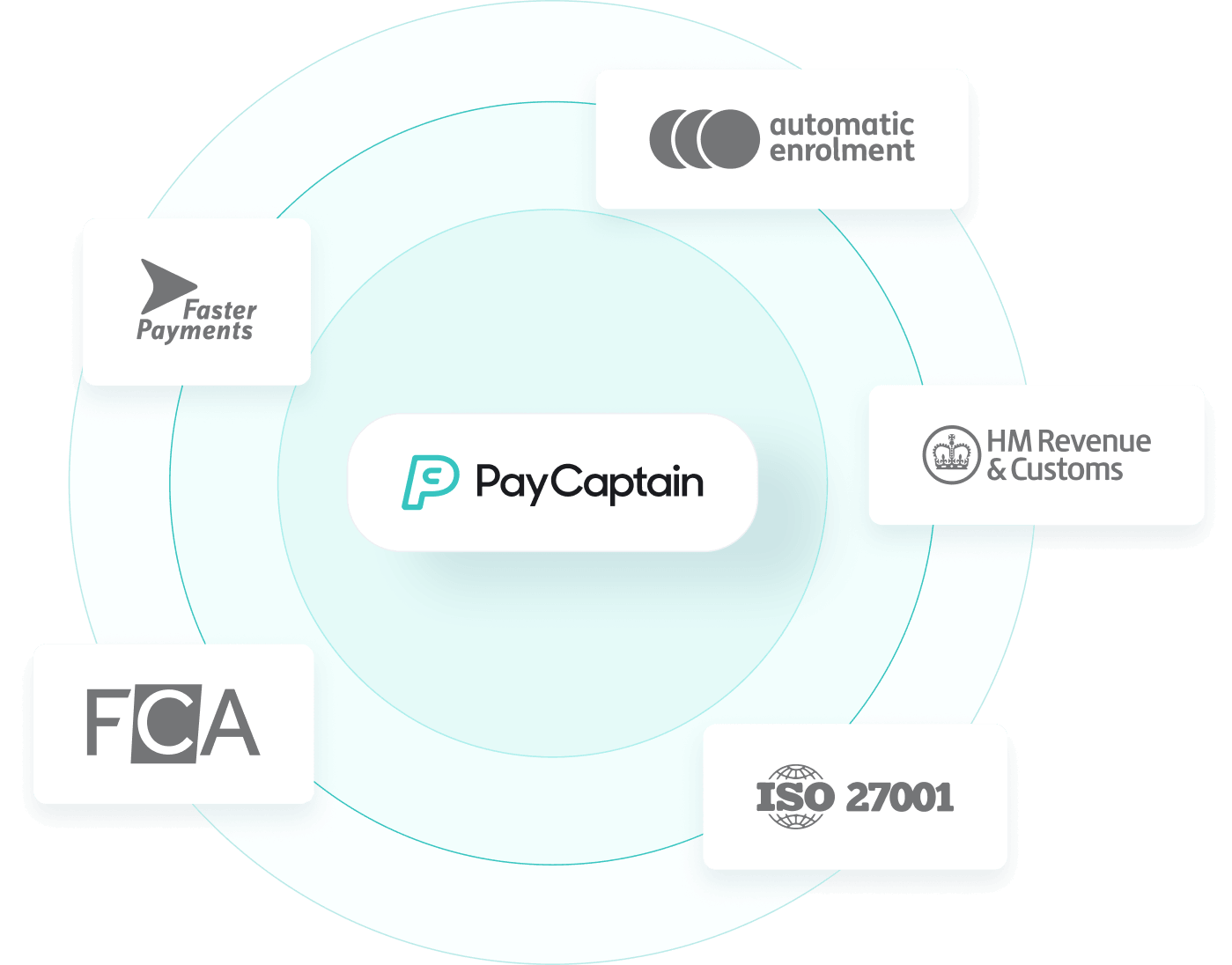

Keeping payroll data safe, secure and fully protected

Keep sensitive payroll data protected and reduce the risk of breaches or unauthorised access. PayCaptain’s payroll reporting software is built with strong security measures, giving employers confidence that employee and financial information is safe.

Safeguard sensitive information, meet legal obligations and maintain trust across the business. PayCaptain is ISO27001 certified - the international standard for information security. All payroll reports are encrypted both in transit and at rest, and access is restricted through role-based permissions. Only authorised users can view or manage payroll data, and every action is logged with full audit trails to support compliance and accountability.

These measures help businesses stay GDPR-compliant, audit-ready and in full control of payroll reporting. With security built in, employers can focus on payroll and their people, confident their data is fully protected.

Are our payroll reports right for your business?

Make better decisions with payroll reports tailored to your business. Whether it's a growing team or a complex enterprise organisation, PayCaptain’s payroll reporting software scales to fit. Custom payroll reports match business goals, team structures and industry needs meaning employers get the right insights. Every time.

Payroll reports that grow with your business

Get the insight you need to plan, manage and grow, no matter how simple or complex your needs. PayCaptain’s payroll software scales with the business, adapting to different team sizes and reporting requirements at every stage.

Small businesses get fast access to essential employee payroll reports that reduce admin and support day-to-day decisions.

Medium businesses benefit from detailed payroll data analysis to manage growing teams and costs.

Large businesses can access advanced payroll dashboards, custom payroll reports and real-time payroll reporting to support strategic planning and compliance.

Enterprise organisations get detailed reports and analytics to strengthen governance, meet compliance requirements and stay audit-ready.

Whatever the size, every business gets the same secure, easy-to-use payroll reporting tools that adapt as things change.

Payroll reports built for your industry

Make smarter decisions, manage staff costs and stay compliant. PayCaptain’s payroll reporting software gives every industry the tools to handle its unique challenges, from shift patterns to workforce changes and sector-specific rules.

In the care sector, employers can stay compliant while managing complex rotas, hourly pay and overtime. Distribution and logistics businesses benefit from real-time insight into shift costs and site-level spend. Hospitality employers get clear, certified payroll reporting to help manage variable hours, seasonal teams and high staff turnover.

HR and recruitment firms use tailored employee payroll reports to manage placements, pay and onboarding processes. In retail and manufacturing, teams can track labour costs by department, monitor site-level spend and improve scheduling with payroll data that’s easy to access and act on.

Whatever the industry, PayCaptain helps employers reduce admin, improve accuracy and take control of payroll performance.

What do our customers think of our payroll reports?

We get better and more detailed information than we’ve ever had before, which of course allows better decision-making. I get virtually unlimited information about our employees and their pay, so when it comes to approving the payroll at the end of the month, my job is very, very simple and easy.

The employee experience is unmatched and the visual reporting makes my life easier when approving things.

Where we’ve needed additional reporting, they have built these within 48 hours.

Frequently Asked Questions

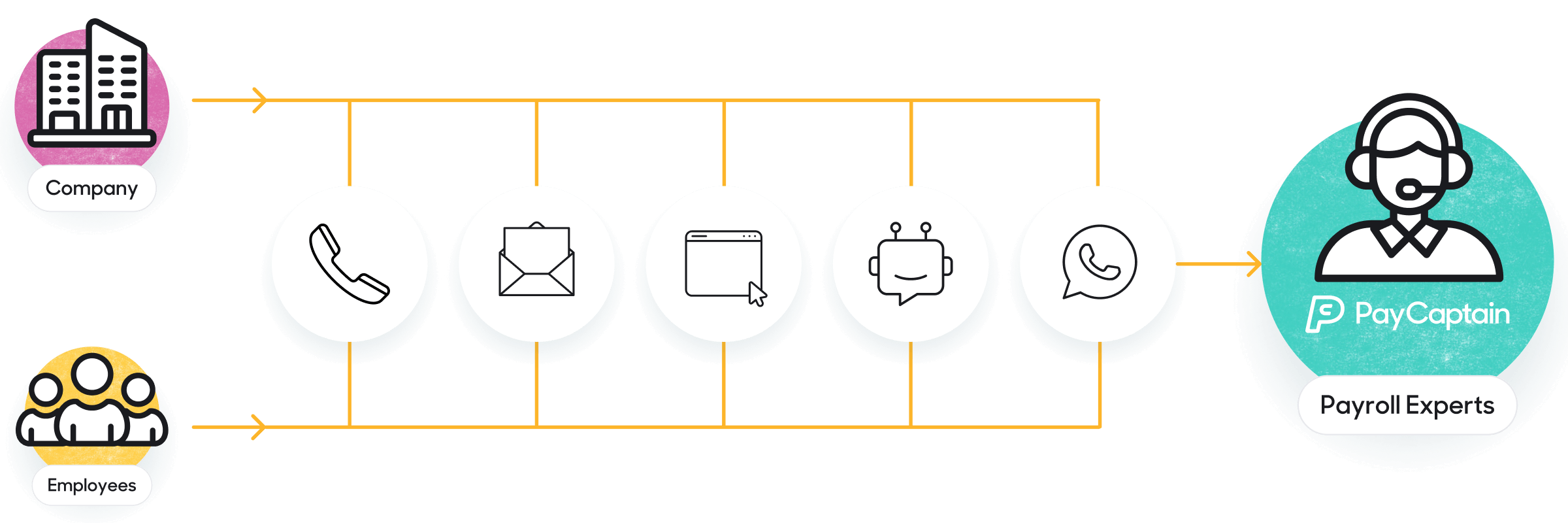

Can I outsource payroll reporting to a third party?

Yes, payroll reporting can be outsourced to a third-party payroll provider. The payroll software provider will manage core tasks such as calculating pay, submitting certified payroll reports to HMRC and producing online payslips. They also generate FPS and EPS payroll reports, helping the employer stay compliant with payroll tax reporting requirements.

Whether the chosen model is hybrid or outsourced payroll, the business should still review and approve employee payroll reports before submission. This includes checking monthly payroll reports, annual payroll reports and custom reports for accuracy. Many businesses use payroll reporting software with a built-in payroll dashboard to access real-time payroll reporting and activity reports for better data analysis.

What are the penalties for late submission of payroll reports in the UK?

HMRC issues penalties for late submission of payroll reports, and the amount depends on the number of employees in the PAYE scheme. Businesses running more than one PAYE scheme may face separate fines for each late submission. Penalties are charged monthly and typically range from £100 to £400 per scheme.

Using payroll reporting software can help avoid missed deadlines by automating key tasks like submitting FPS and EPS reports. PayCaptain includes certified payroll reporting as part of its standard service, ensuring all mandatory online payroll reports are submitted to HMRC on time. This reduces the risk of penalties and gives employers peace of mind with accurate, real-time payroll reporting.

What monthly payroll reports should be submitted to HMRC?

Employers must submit a Full Payment Submission (FPS) every time employees are paid. An Employment Payment Summary (EPS) is also required, usually by the 19th of the following tax month. These monthly payroll reports help HMRC track pay, tax and National Insurance contributions.

Most businesses use payroll reporting software or an outsourced payroll provider to manage these submissions accurately and on time. This ensures compliance with HMRC annual payroll reporting rules and reduces the risk of errors.

What is gender pay gap reporting?

Gender pay gap reporting is a legal requirement for employers with more than 250 employees. It involves submitting annual payroll reports that show the average pay difference between men and women in the workforce over a set period. The data must also be published clearly on the employer’s website by a set deadline.

These reports form part of wider payroll reporting duties and help highlight pay inequality for similar roles. Gender pay gap reporting software is a standard feature of PayCaptain’s reporting function.

What types of reports can payroll software generate?

Payroll reporting software can run a wide range of reports to help employers stay compliant and make informed decisions. Common types include payroll activity reports, employee payroll reports, and HMRC-ready submissions like FPS and EPS. It also supports both monthly and annual payroll reports for financial tracking and tax purposes.

PayCaptain offers online payroll reports with a real-time payroll reporting dashboard. Employers can also create custom payroll reports for specific needs, such as payroll data analysis or gender pay gap reporting. These features help improve accuracy, visibility and control across the payroll process.

How does payroll reporting software help with financial forecasting and budgeting?

Payroll reporting software gives employers access to real-time payroll reporting and accurate payroll data analysis. This helps finance teams track salary costs, monitor trends and plan for future payroll spending with more confidence. It also reduces guesswork by generating monthly and annual payroll reports that feed directly into cashflow forecasts.

Online payroll reports and custom payroll reports can show patterns in overtime, bonuses and staff turnover. These insights support better decision-making across budgeting, hiring and resource planning. For more detail, see PayCaptain’s guide to payroll and financial forecasting.

How does real-time payroll reporting benefit businesses?

Real-time payroll reporting gives employers instant access to up-to-date payroll data. This means errors can be spotted early, employee payroll reports can be checked before payday and compliance issues can be avoided. It also supports faster decision-making by providing current figures on pay, tax and deductions.

With a payroll dashboard offering real-time insights, businesses can monitor payroll activity reports throughout the month rather than waiting for end-of-period summaries. This improves accuracy. It results in better payroll management reports and helps the business stay in control of cashflow.

Start making payroll a breeze

We'd love to talk about how PayCaptain can add value to your company and your employees. Click the button below to arrange a demo and see PayCaptain in action!

Latest insights

How payroll APIs connect modern payroll systems

Learn how payroll APIs enable modern payroll platforms to integrate with HR and finance systems.

Common HRIS and payroll integration architecture models

Explore the common ways HR systems integrate with payroll platforms and why architecture decisions matter.

%20200.png)

Payroll governance frameworks and what large organisations need in place

Learn what a strong payroll governance framework looks like and how organisations manage risk, approvals and accountability at scale.