A good payroll reconciliation process shows that payroll, finance, HRIS data, RTI submissions and bank payments all agree. It also gives auditors clear payroll audit evidence, including locked payroll reports, FPS timestamps, liability roll-forwards and signed reviews.

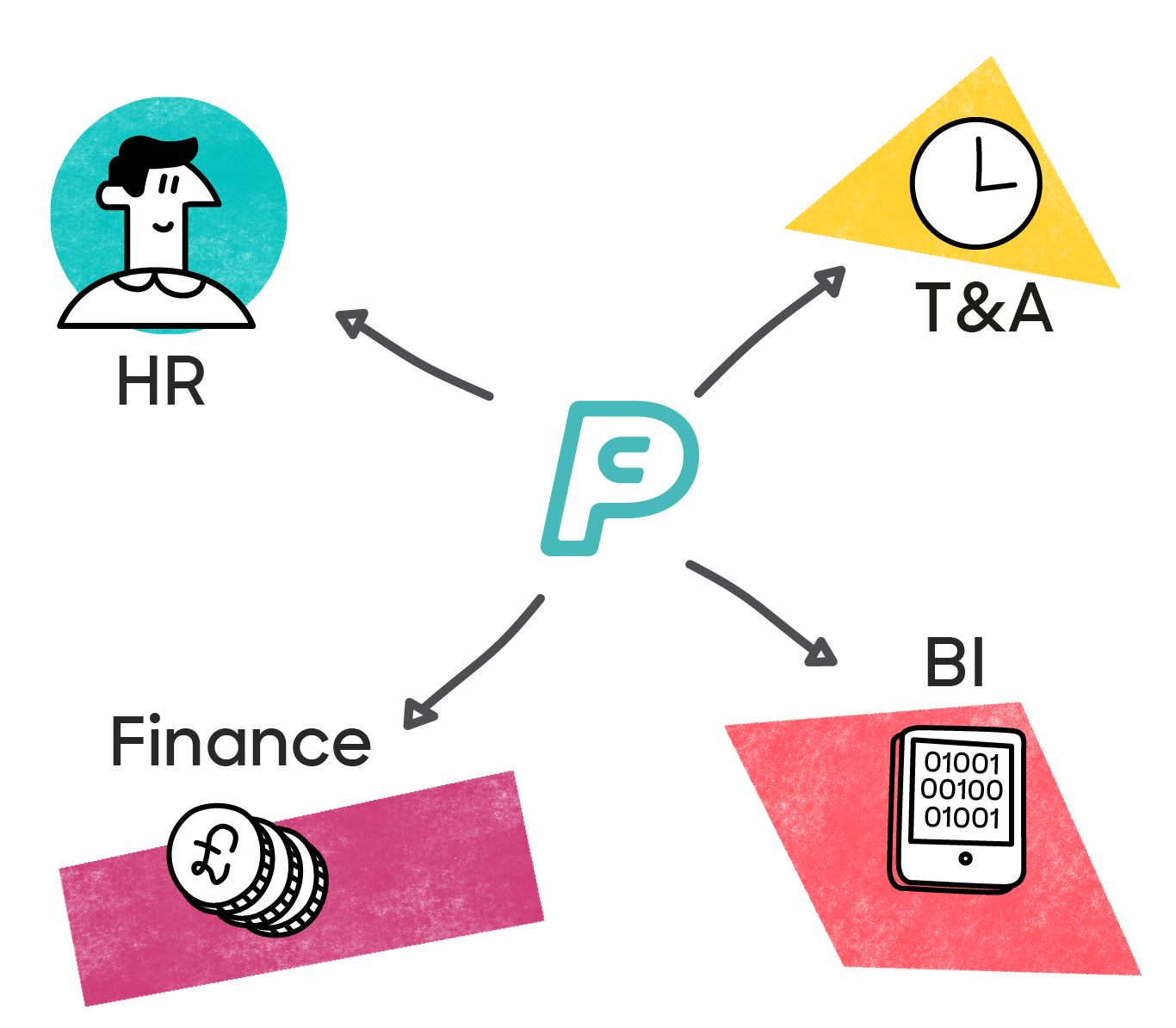

Payroll reconciliation is the process of checking that payroll figures match across the systems and records used by the business. For enterprise payroll, this means checking pay, deductions, HMRC reporting, journals, payments and liabilities.

Payroll doesn’t operate in isolation:

- Employee information starts in an HR system

- Working hours may come from time and attendance

- Pension data needs to be shared with providers

- Payroll costs need to reach finance systems

- Statutory information must be reported to HMRC

For payroll reconciliation to work well, all of these records need to tell the same story.

Contents

What enterprise payroll reconciliation involves- Why payroll reconciliation risk grows as organisations become more complex

- What good payroll reconciliation practice looks like

- Payroll audit evidence auditors expect to see

- Common payroll reconciliation errors and how to prevent them

- How payroll technology supports reconciliation and audit readiness

- Final thoughts from PayCaptain on good enterprise payroll reconciliation

What enterprise payroll reconciliation involves

Payroll reconciliation checks that the payroll result matches the records around it.

For smaller organisations, this may be easier to see in one place. As organisations grow, payroll usually becomes more connected and more complex. Data may come from HRIS, time and attendance systems, benefits platforms and finance systems before the final payroll is confirmed.

At enterprise scale, payroll reconciliation means checking several key records against each other.

This can include:

- gross pay and deductions

- net pay and bank payment totals

- final payroll register totals

- payroll journals posted to the general ledger

- Full Payment Submissions and other RTI returns sent to HMRC

- PAYE and National Insurance liabilities

- pension contribution balances

- off-cycle payments and corrections

The aim is to make sure the final payroll position is accurate. It also needs to be authorised and traceable.

- the payroll register should agree with the payroll journal

- the FPS sent to HMRC should match the final payroll data

- the bank payment file should match net pay

- PAYE, NIC and pension liabilities should also move in a way finance can explain.

Payroll reconciliation isn’t just a payroll check. It’s part of the wider control environment that helps finance understand payroll costs and helps the business prove what was reported to HMRC.

Explore payroll with PayCaptain

Why payroll reconciliation risk grows as organisations become more complex

Payroll risk grows when there are more systems, pay groups and people involved in the process, so the payroll control model must match the size and shape of the business.

A large employer may operate more than one PAYE scheme. They may run weekly and monthly payrolls at the same time and parts of the business may have different rules for overtime, shift premiums, commission, bonuses or salary sacrifice. This is particularly the case where irregular hours or part-year workers are involved. Each layer of complexity creates more places where data can be late, missing or wrong.

Many payroll reconciliation errors begin before payroll is processed. They often come from HR workflows or line manager submissions. They can also come from gaps between HRIS and payroll systems. Examples include:

- a starter may be added late

- a leaver form may arrive after the cut-off

- a manager may approve hours too close to payroll processing

- an integration may move data from one system to another, but not in the way payroll needs it

Payroll may then calculate correctly using data that was already wrong.

This is why payroll reconciliation needs to look beyond the pay run itself. It should help the organisation see where data is breaking before it reaches payroll.

How clear ownership reduces payroll reconciliation risk

Payroll often becomes the place where upstream problems are found. This can create pressure for payroll teams because they’re asked to fix issues they didn’t cause. The better control outcome is clear ownership across the process.

Typically:

- HR owns employee records

- Managers own approvals and cut-offs

- Payroll owns payroll processing and statutory reporting

- Finance owns journals and liability review

- IT owns system access and integration reliability

When ownership is clear, payroll reconciliation can show where issues are coming from and who needs to help resolve them. When ownership is unclear, reconciliation can turn into a monthly search for answers.

What good payroll reconciliation practice looks like

Good payroll reconciliation practice is structured and repeatable.

It shouldn’t depend on one person remembering what happened last month or on a spreadsheet only one person understands. It should create a clear record that another trained person can follow.

At enterprise scale, good payroll reconciliation usually includes:

- a locked final payroll register

- journals based on final payroll data

- clear posting logic

- liability roll forwards for PAYE, NIC and pensions

- checks that Scottish and Welsh tax codes have been applied correctly where the workforce spans multiple UK tax jurisdictions

- bank payments matched to net pay

- exception logs for corrections and off-cycle payments

- preparer and reviewer sign-off

- evidence stored for audit review

The process should make it clear which differences are timing issues and which are true errors. A timing difference may be valid. An unexplained balance needs review and closure.

Each level should be closed before the next one is relied on so the final payroll register becomes the source of truth.

- the payroll journal then ties back to the register

- payroll costs are posted to the right period

- liabilities are rolled forward

- cash payments are checked against payroll obligations

Exceptions then follow the same control route. They don’t sit outside the process.

This makes payroll reconciliation easier to repeat. The team is not working out how to prove the numbers each month. They are following a known route and keeping payroll audit evidence as they go.

Why good payroll reconciliation needs a clear audit trail

Delayed or incomplete reconciliations often happen when too much knowledge sits with one person. It can also happen when the team is under pressure and there’s no documented process.

- if the reconciliation depends on memory, the process is fragile

- if an auditor needs one person to explain the story, the evidence is not strong enough

A better process leaves a clear trail, showing what happened and who reviewed it. It should also show what’s outstanding for resolution.

Payroll audit evidence auditors expect to see

Auditors expect payroll audit evidence that proves the control has happened. They don’t just want to know that payroll has been checked - they want to see what was checked, by whom and when.

A strong payroll close pack may include:

- the final payroll register export

- the payroll journal posted to the general ledger

- FPS confirmation and timestamp

- bank reconciliation for net pay

- PAYE and NIC liability roll forward

- pension contribution reconciliation

- exception log for the period

- preparer and reviewer sign-off

The payroll reconciliation evidence doesn’t need to be complicated – just complete and easy to follow.

A reviewer should be able to trace a payroll figure back to its source without rebuilding the month from emails and spreadsheets. If they can’t, the payroll reconciliation control isn’t strong enough.

HMRC payroll records and retention requirements

HMRC-related payroll audit evidence includes FPS records, EPS receipts, payslips, P45s, P60s and P11Ds. Tax code notices also need supporting evidence. The organisation should be able to show that the notice was applied correctly and in the right pay period.

For records needed for National Minimum Wage, evidence needs to include time records, attendance data and pay calculations. This helps show that workers have had their wages calculated correctly.

Record retention needs the same discipline:

- PAYE records must be kept for at least three years after the end of the relevant tax year

- National Minimum Wage records must be kept for six years — this has applied to pay reference periods since April 2021, up from the previous three-year requirement

- Pension auto-enrolment records must be kept for six years, except opt-out notices, which only need four years

Because these minimums differ by record type, some larger organisations choose a single six-year baseline across all payroll-related records rather than tracking separate periods - this is a discretionary simplification, not a requirement.

Common payroll reconciliation errors and how to prevent them

Many payroll reconciliation errors fall into familiar areas.

Some relate to incorrect employee data. Others come from late starters, missed leavers, old tax codes, incorrect student loan plan types, benefit deductions or general ledger mapping. Some happen because payroll has been reconciled against preview data instead of the final payroll register.

Common causes include:

- manual re-keying between systems

- HRIS and payroll fields not matching

- late manager approvals

- leaver forms arriving after payroll cut-off

- HMRC tax code notices not applied on time

- student loan plan type or start/stop notices not applied correctly

- benefit changes not reflected in payroll

- chart of accounts mapping changes

- Apprenticeship levy calculations not reviewed against the annual allowance

- journals posted from preview payroll data

Payroll reconciliation errors aren’t always payroll calculation errors.

If starter data keeps arriving late, payroll will keep dealing with late changes. If leaver forms are not controlled, overpayments can keep appearing. More checking at the end may catch the issue, but it won’t fix the source.

How upstream data issues affect payroll reconciliation

The strongest way to reduce payroll reconciliation errors is to improve data before it reaches payroll.

To stop the issue repeating, the focus needs to move upstream. Payroll teams need accurate data before the pay run starts. This means setting clearer cut-offs and making ownership easier to see. It also means removing manual handoffs as data moves between systems.

Payroll reconciliation can become a source of insight, showing where data issues are starting and where the wider process needs attention.

Why exception logs matter in payroll reconciliation

Off-cycle payments, back pay, reversals and corrections all increase reconciliation risk as they happen outside the usual rhythm of payroll.

A good exception log should show what happened and which pay run was affected, as well as who approved the change and how it was treated in the accounts. This helps keep the main payroll reconciliation clean. It also gives auditors a clearer record to review.

How payroll technology supports reconciliation and audit readiness

Modern payroll technology makes payroll reconciliation easier to manage as organisations grow.

It can help move approved data between systems using secure integrations. It supports variance checks, audit trails, access controls and exception reporting. It also reduces manual handoffs between HRIS, payroll and finance systems.

This is where cloud payroll software delivers stronger reconciliation outcomes. The aim is better control over payroll data and clearer evidence when the business needs to prove the numbers.

For example, AI powered variance checks can flag unusual pay movements, zero net pay or first payments to new bank details. This helps payroll teams focus on records that need attention.

System audit trails can also strengthen payroll audit evidence. They can show who made a change, when it happened and what the value was before and after.

This technology gives internal and audit teams a stronger record than a spreadsheet that can be edited or overwritten.

Make payroll reconciliations easier to prove

Why connected systems make payroll reconciliation easier

Payroll reconciliation is harder and riskier when teams need to move data manually between platforms. Connected systems reduce rekeying. They also reduce the risk of different teams working from different versions of the same employee record.

This is where payroll integrations support enterprise payroll controls. When approved data moves between HR, payroll and finance in a controlled way, reconciliation has a better starting point.

Why payroll technology still needs governance

Technology can improve the payroll reconciliation process, but it doesn’t replace governance.

An integration can move data from HRIS to payroll, but it can’t decide whether the data is complete or accurate. It can’t replace clear ownership or human review.

Automated checks can help payroll teams spot exceptions sooner and flag them for human review. The exceptions still need people to review the reason. They can then decide the next step and record the outcome.

Technology works best when it supports clear enterprise payroll controls. The outcome is a payroll reconciliation process that’s easier to run and prove.

Final thoughts from PayCaptain on good enterprise payroll reconciliation

Good payroll reconciliation gives organisations a clearer view of payroll risk. It shows whether payroll, HR and finance are working from the same information and helps teams see where errors are really starting.

It’s one of the most useful parts of the process. Payroll reconciliation doesn’t just prove the numbers. It can also show whether poor data or unclear ownership is creating repeat issues - those that, left unresolved, can lead to late or inaccurate RTI submissions and the HMRC penalties that come with them.

For auditors, the question is simple.

Can they follow the payroll output back to the source without rebuilding the month? If they can, the process is in a much stronger position. If they can’t, the organisation may be relying too much on memory and workarounds.

A good payroll reconciliation process should leave a clear trail It should give auditors the payroll audit evidence they expect and help organisations reduce errors by fixing the issues that cause them in the first place.

When payroll information moves through the business in a controlled and reliable way, payroll teams spend less time chasing differences and more time making sure payroll is correct, on time, every time.

Frequently asked questions about payroll reconciliation

What is payroll reconciliation?

Payroll reconciliation is the process of checking that payroll figures match across payroll records, finance systems, bank payments and HMRC submissions.

What evidence do auditors expect for payroll reconciliation?

Auditors usually expect payroll audit evidence such as the final payroll register, payroll journals, FPS timestamps, bank reconciliations, liability roll forwards and exception logs.

How can large organisations reduce payroll reconciliation errors?

Large organisations can reduce payroll reconciliation errors by improving the data before it reaches payroll. This includes clearer ownership, stronger cut-offs and better connections between business- critical systems.

Strengthen payroll reconciliation and audit readiness

.png)